Deep Dive into Managed Care Organizations (MCOs), part 1

Evolution of MCOs and why they are still attractive

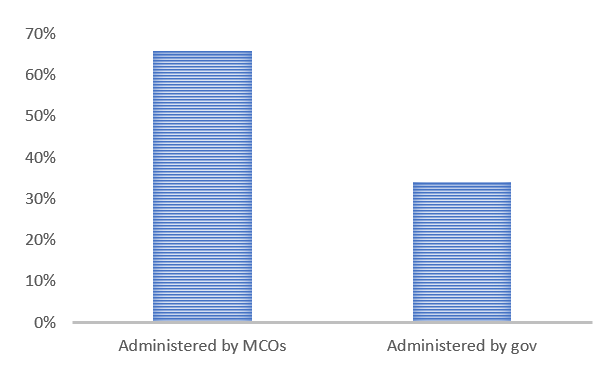

Breakdown of healthcare $

Before diving deep into MCOs, here’s a helpful breakdown first of healthcare dollars spent in the US. It is oft-quoted that the US spends 18% of GDP on healthcare, right? So, that’s ~$4 trillion. Of that $4tr, 75% or $3tr comes from healthcare insurance (remainder is out-of-pocket and 3rd party). This $3tr is broken down below:

Commercial insurance is what is provided to employees by companies and is $1.3tr, Medicare is a government entitlement program provided to 65+ individuals is $0.9tr, Medicaid is another government entitlement program provided to low-income individuals and those with disabilities is $0.6tr, and other government programs like Veterans Affairs is $0.1tr. Collectively, 56% of healthcare $ come from the government and the remaining 43% from companies.

The more important distinction for this discussion is how much of these healthcare $ flow through MCOs versus the government and the answer to this is 66% versus 34%.

What are MCOs anyways?

As you may have surmised from above, MCOs are companies that administer healthcare $ by paying for healthcare costs generated by individuals they cover when said folk go to the doctor for a checkup, the hospital for surgeries, the lab for running tests, and the pharmacist for medicines. To balance paying for these costs, MCOs collect premiums for the individuals they cover. Note that in the US, this is largely a utility-like business in that gross margins are capped at ~15% with some exceptions but scale can still help generate a higher operating margin through lower operating costs like selling, general & administrative.

What do I mean by exceptions? Well, government entitlement programs are complicated and in an effort to shift from fee-for-service to fee-for-value, the government provides additional incentives if the MCO delivers higher-quality care. For eg., an MCO that provides high-quality Medicare service can effectively have double their margin via incentives offered.

When I said that MCOs administer healthcare $, this was an understatement worth unpacking a little further. MCOs do collect premiums from companies or the government on behalf of individuals and then pay for healthcare costs that arise but they usually have an active say in what plan characteristics (ie., what benefits they will cover) and can help lower the cost of healthcare by steering individuals to lower-cost healthcare providers like urgent care centers versus hospitals. These networks can include thousands of nodes on a national level so establishing and maintaining these nodes acts as a barrier to entry.

The other theme you may have noticed recently with MCOs is that they are vertically integrating with other parts of the healthcare value chain like healthcare providers including physicians, pharmacy benefit managers, and pharmacies. Why you may ask? One reason is that controlling these assets may help offer higher quality care (so higher revenues by qualifying for incentives for higher-quality care) and lower the cost of care through things like more effective steering (also higher revenues as can offer more competitive plan rates than peers that should attract more business). Another reason is that these are not margin-regulated businesses in the way that healthcare insurance is so ownership of these assets is an opportunity to increase consolidated company margins. For eg., UnitedHealth has some software and data analytics type businesses within their mix that have 4x the margins as their insurance business.

How did such a convoluted system evolve?

Health insurance in the US began as an experiment in 1929 in Texas. At the time, Baylor University Hospital was dealing with falling occupancy rates and patients who were unable to pay their own bills. The hospital devised a ‘prepaid hospital coverage plan’ that gave teachers 21 days of hospital care for $6/yr. This prototypical non-profit insurance plan spread quickly to other employee groups and to other States and was eventually modified such that coverage would encompass several hospitals rather than just one. This type of plan adopted the name of Blue Cross in 1938 and was endorsed by the American Hospital Association. By 1940, 6 million people across the country were covered under Blue Cross plans.

World War 2 was a catalyst for further adoption of health insurance by employers. This is because the Stabilization Act of 1942 froze wages and prices to counter inflationary pressure during this era and so, employers turned to employee benefits like health insurance to attract good talent. So, while before World War 2 only 10% of employees had health coverage, by 1955, 70% of employees had health coverage.

Government role in healthcare insurance was expanded in the 1960s with the enactment of Medicare and Medicaid, which were described above. And in 2010, Medicaid in particular was further expanded under the Affordable Care Act as more people were now eligible for more benefits under the plan.

Where does the system stand now?

Clearly, the healthcare system in the US is bloated. US healthcare expenditure is 18% of GDP vs 10-12% for most other developed countries. There is little to indicate as well that the excess spend results in correspondingly better healthcare as the US is worse than other developed countries on several healthcare indicators like mortality rates and arguably, the gap is getting wider. The caveat is that it is difficult to tease apart specific impact of healthcare delivery versus other intervening variables like socioeconomic status and lifestyle choices.

How do you increase efficiency in an opaque and fragmented system? Simple, you centralize it as other developed countries have done. But, this is a politically unpopular option. Another option with much less political opposition so far is to shift healthcare $ over to MCOs (ie., outsource) allowing them to gain bargaining power and control costs. This has gained traction as more of Medicare and Medicaid $ have shifted over to administration by MCOs through Medicare Advantage and Managed Medicaid programs, respectively. ~40% of all eligible Medicare members have Medicaid Advantage plans that are administered by MCOs and ~70% of eligible Medicare members have Managed Medicaid plans that are administered by MCOs and penetration of both of these types of MCO-administered plans is continuing to grow rapidly.

Where do we go from here?

As a result of the above-mentioned forces (ie., outsourcing and vertical integration), the MCO industry has gotten more consolidated over time and more vertically integrated over time. It is an attractive industry with high barriers to entry, high bargaining power for the larger players (local market shares are typically 30+% for the big three), and favorable secular trends (aging demographics, more outsourcing). Balancing that is the stroke of pen risk or regulatory risk that MCOs could become extinct if healthcare is centralized, again a politically unpopular option. The contrarian view here may be that MCOs are viewed as just healthcare insurers, which historically was a capital intensive and risky business. However, MCOs have evolved to now being administrators rather than risk bearers (ie., less capital intensive and less risky) and through vertical integration, a large portion of their overall business is not related to healthcare insurance.

Please subscribe as I’ll be posting part 2 soon where I’ll discuss the largest MCOs, UnitedHealth, Anthem, and CVS, in more detail.