Deep Dive into Cable Companies, part 2

Why $CABO and $CHTR are attractive opportunities here

In part 1, we looked at the evolution of cable’s business model over time and why the industry is still attractive despite disruptive and regulatory threats. In this part, we’ll take a closer look at the main players in the cable industry, Charter, Comcast, Altice, and Cable One.

One difference right off the bat is in the size of these companies as illustrated below. Another difference is business diversification with Comcast being the only player that is not a cable pure-play as 30% of its business is content production and theme parks (ie., under the NBC Universal banner).

How do these companies make money?

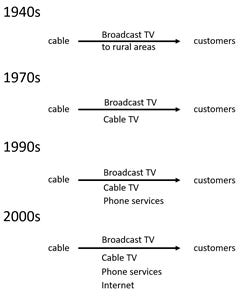

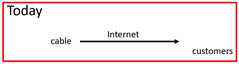

As discussed in the last note, cable was a bundle of services that included high-speed internet, TV, and phone services but the bundle has been losing popularity as streaming services and wireless phone service substitute for TV and (landline) phone services. Counter-intuitively, the slow decline of TV and phone services is not bad for cable companies as: 1) this allows them to raise their price of high-speed internet on an unbundled basis; 2) high-speed internet is higher margin and lower capex intensity than video as there are no content (aka programming) costs and fewer hardware and maintenance costs to bear for internet. This is why cable companies claim that FCF/customer is growing for them even as TV and phone services decline.

As high-speed internet is the key high-value service offered by cable companies, it’s helpful to examine this in particular across the companies.

Clearly, there is a large difference across the cable companies in terms of internet subscribers, and a small difference in what they charge/subscriber/mon. On the second point though, companies may have a different way of allocating revenues to specific services (eg., how much of the bundle price is allocated to internet vs video vs phone services may vary across the companies).

An important difference to note is that the cable companies play in different geographies essentially giving them a monopoly or duopoly status for high-speed internet across ~90% of subscribers served. One nuance is that Altice has a weaker competitive position relative to peers as ~1/3rd of the subscribers it serves also overlap with Verizon’s Fios service, which also provides high-speed internet (vs ~10% of subscribers for Comcast and Charter and ~0% for Cable One). An offset though is that Altice’s subpopulation of subscribers are relatively affluent and more willing to bear a higher price, which is perhaps what is reflected in their industry-leading rev/sub/mon (aka ARPU). Another such nuance is that Cable One serves semi-rural areas and as such, faces less competition than its peers that largely focus on urban and suburban areas. This may also help explain a relatively high ARPU for Cable One versus Comcast and Charter.

Who’s the greatest cable cowboy of them all?

I’d be remiss to not talk about management of these cable companies by their respective cable cowboys, a term coined by author Mark Robichaux who wrote a book on the one of the greatest cable cowboys, John Malone. The title for greatness probably goes to both John Malone, the founder of Charter Communications, and to Patrick Drahi, the founder of Altice. And no surprise, these are two of the richest men in the cable business. Patrick was John’s protégé and is a more extreme version of him in the aggressiveness with which he uses leverage to make deals or to buy back shares.

Comcast is led by Brian Roberts, son of Comcast’s founder and like a true second generation family owner, he’s “de-worsified” the original cable business with a content business that is now struggling to make the transition from linear TV to streaming services. Brian still stands by his decision to buy Sky in a bidding war against Fox at arguably, the peak of the cycle and most recently, is rumored to be once again looking for other content assets to further scale up the business. In my view, diluting what is an excellent cable business with content business that is just ok is the incorrect strategy to take and to do it with little regard to return on invested capital is worse. For his efforts, he gets the label of the worst cable cowboy.

Cable One, in contrast, has a more traditional corporate culture with senior mgmt. that is less tenured than at peers but still competent. They’ve stuck to their knitting of focusing on acquiring cable companies operating in semi-rural areas with limited competition. As one positive indicator of mgmt’s ability to allocate capital well, Cable One has the highest return on invested capital of the cable companies.

How does valuation compare?

Generally, the FCF yield and forward P/E metrics agree that Cable One is the most expensive cable company while Altice is the cheapest. Keep in mind that Comcast is not an apples to apples comparison with the other cable companies as arguably, the content portion of its business should be valued at a lower multiple than cable.

To me, valuation for the pure-play cable companies seems relatively efficient and reflects a high-quality, defensive business in both Cable One and Charter with additional upside in Cable One from continued roll-up of semi-rural cable companies (there are ~50m homes that are not currently canvased by the largest cable companies and many of them are likely in rural and semi-rural areas that Cable One is targeting) and in Charter from margin expansion (EBITA margin is ~30% lower than that of Altice and Cable One for eg. but steadily growing over time). If you assume Altice-like margins for Charter, then the valuation multiple gap between the two companies shrinks to about 5x versus ~16x currently. Again, in my perspective, this is a reasonable discount for Altice given a more competitive footprint and a more aggressive capital allocator that is willing to lever up to an extreme.

What’s the best play here?

In my opinion, Charter and Cable One represent the best opportunities in cable as they are relatively high quality assets with good management teams that have good growth potential ahead of them. You could especially argue for a variant perception on Cable One, which because it is much smaller doesn’t get nearly as much coverage as Charter, Comcast, and Altice get.